Bookkeeping for Self-Employed Made Simple

Quick Takeaways – Bookkeeping for Self-Employed:

- Open a separate business bank account first — IRS Publication 583 recommends it, and it cuts your time in half

- Use cash basis accounting if you’re under $31 million in revenue (you are)

- 30 minutes a week of categorizing transactions keeps tax season from becoming a crisis

- Self-employment tax is 15.3% on top of income tax — set aside 25–30% of every payment received

- The 2026 quarterly tax deadlines are 15 April, 15 June, 15 September, and 15 January 2027

- Most freelancers under $100K in revenue can DIY; above that, a bookkeeper at $200–$400/month usually pays for itself — especially when your bookkeeping for self-employed workload starts to grow

Nobody becomes a freelancer because they love reconciling bank statements.

You started your business to do work you care about, get paid for it, and skip the 9-to-5. But then tax season shows up, and suddenly you’re knee-deep in receipts, wondering where $3,000 went last March.

It doesn’t have to be like this.

Bookkeeping for self-employed people is simpler than most guides make it sound. You need a system, about 30 minutes a week, and a basic understanding of what the IRS expects. This guide covers all three.

What Does Bookkeeping for Self-Employed Actually Mean?

Bookkeeping is tracking every dollar that comes in and goes out of your business so you can file accurate taxes, claim every deduction you’re owed, and actually know if you’re making money.

When you worked for someone else, your employer handled tax withholding, paid half your Social Security and Medicare, and gave you a W-2 at the end of the year.

Now?

All of that is on you.

You’re tracking income, categorizing expenses, paying your own taxes quarterly, and keeping records the IRS can audit at any time.

Sounds overwhelming. It’s not, once you have a system.

First decision: cash basis or accrual?

Almost every freelancer should use cash basis accounting.

You record income when you receive it and expenses when you pay them. It mirrors your bank account, it’s simpler, and the IRS allows it for any business under $31 million in revenue.

So you probably qualify.

Second decision: software or spreadsheet?

Either works.

If your finances are still straightforward, managing your small business accounting in Excel can be enough — as long as you use consistent categories and update the spreadsheet regularly.

But accounting software (Wave, QuickBooks, FreshBooks) runs double-entry bookkeeping behind the scenes while showing you a simple dashboard.

You don’t need to understand debits and credits. The software handles it.

That’s exactly why modern tools make bookkeeping for self-employed people much easier to manage.

If you want help choosing the right tool, check out our guide to the best accounting software for freelancers.

But before anything else, do this one thing: open a separate business bank account. IRS Publication 583 recommends it explicitly.

It’s the single most impactful step you can take. Mixing personal and business transactions turns bookkeeping from a 30-minute weekly task into a multi-hour monthly nightmare.

What Records Matter in Bookkeeping for Self-Employed?

The IRS requires you to keep records that support every income and expense item on your tax return, and you need to hold onto them for at least three years. Seven is safer.

Per IRS Publication 583, your records should include gross receipts documentation (invoices, 1099 forms, bank deposit records), expense records with business purpose noted (receipts, canceled checks, credit card statements), and asset records for anything you depreciate (computers, equipment, furniture).

Good bookkeeping for self-employed individuals means keeping these records organized and accessible at all times.

Quick note here: the IRS doesn’t require receipts for individual expenses under $75, except for lodging. That said, keep everything anyway. Digital counts. Photos of paper receipts, downloaded bank statements, email confirmations from vendors. All valid.

How long do you need to keep this stuff?

The IRS says three years from the date you file. But if you underreport income by more than 25%, that extends to six years. For bad debt deductions, seven years. And if you never file or file fraudulently, there’s no limit.

The practical move? Keep everything for seven years and stop thinking about it.

This simple habit alone strengthens your entire bookkeeping for self-employed system.

The easiest way to stay on top of records? That separate business bank account again. If the IRS audits you and your business expenses are tangled with grocery runs and Netflix, you’ve made their job easy and yours miserable.

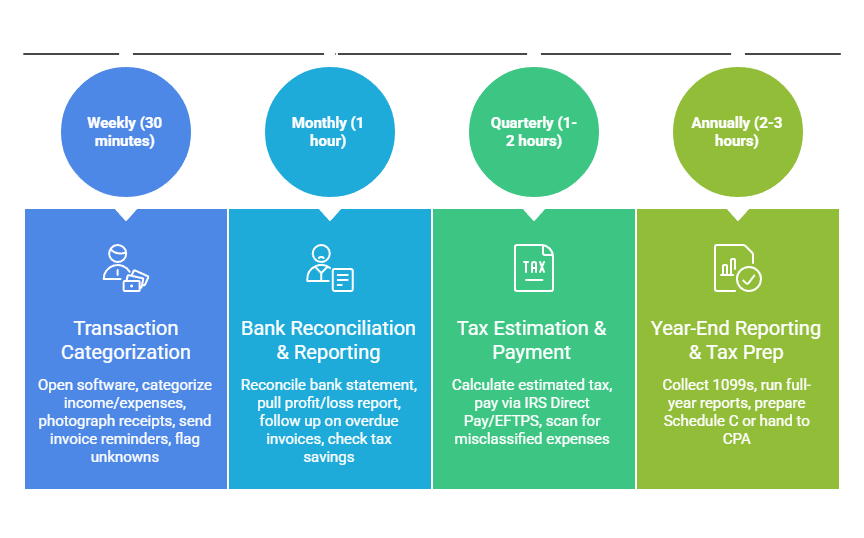

What Does a 30-Minute Weekly Bookkeeping Routine Look Like?

Set aside 30 minutes once a week to categorize transactions, snap photos of receipts, and flag anything unusual. Do this consistently, and tax season becomes a non-event.

Bookkeeping only becomes painful when you let it pile up. A shoebox of receipts in April is a problem. A weekly habit in real time? That’s just maintenance.

That consistency is what makes bookkeeping for self-employed feel effortless over time.

Pick a day. Stick to it. The routine looks like this.

Every week (about 30 minutes): open your accounting software or spreadsheet, categorize any new income and expenses from the past seven days, photograph any paper receipts and attach them to transactions, send reminders on any overdue invoices, and flag anything you’re unsure how to categorize.

Don’t agonize over it. Just mark it and ask your accountant later.

At the end of each month (about an hour): reconcile your bank statement against your records, pull a profit and loss report to see where you actually stand, follow up on any outstanding invoices past 30 days, and check whether you have enough set aside for your next quarterly tax payment.

Each quarter (an hour or two, before tax deadlines): calculate your estimated tax payment, pay via IRS Direct Pay or EFTPS, and scan for misclassified expenses.

Once a year: collect 1099s from clients, run your full-year reports, and either prepare your Schedule C or hand everything to your CPA. If you’ve done the weekly work, this takes a couple of hours instead of a couple of weeks.

Which Deductions Are Most Freelancers Missing?

Home office, mileage, health insurance premiums, and retirement contributions are the four deductions that save the most money. Most freelancers either skip them or undercount them.

These aren’t obscure tax tricks. They’re legitimate deductions built into the tax code for self-employed people. But you have to track them properly.

Home office. Two methods:

- Simplified — $5 per square foot, max 300 sq ft, for up to $1,500/year

- Actual expense — deduct a percentage of real housing costs based on your office’s share of total space. E.g., 150 sq ft office in a 1,500 sq ft apartment = 10%. If rent, utilities, and insurance total $24,000/year, your deduction is $2,400.

- You can switch methods each year.

Mileage. The 2026 IRS standard rate is 72.5 cents per mile.

- 10,000 business miles = $7,250 deduction

- You need a log with the date, destination, and business purpose of each trip

- Apps like MileIQ or Everlance can automate this entirely

Health insurance. Self-employed people can deduct 100% of health, dental, and vision premiums for themselves and their dependents.

- It’s an above-the-line deduction — no need to itemize

- $12,000/year in premiums = $12,000 off your taxable income

Retirement contributions. A SEP IRA lets you contribute up to 25% of net self-employment earnings.

- 2026 cap: $72,000

- A freelancer earning $60K net could shelter roughly $12,000 pre-tax

Other deductions people forget:

- Software subscriptions

- Professional development courses

- Business insurance

- Business-use percentage of your internet bill

- Payment processing fees (Stripe, PayPal)

If it’s ordinary, necessary, and documented, it probably counts. Check the Schedule C instructions for the full list.

Quarterly Taxes and Bookkeeping for Self-Employed

If you expect to owe $1,000 or more in taxes for the year, the IRS requires you to pay estimated taxes four times a year: April, June, September, and January.

This is what catches first-year freelancers completely off guard. Not just income tax. Self-employment tax, too.

The self-employment tax rate is 15.3% (12.4% Social Security plus 2.9% Medicare). On $80,000 in net profit, that’s roughly $11,300 in SE tax alone, on top of income tax. When you were an employee, your employer paid half.

Now you pay all of it.

The 2026 quarterly due dates are April 15, June 15, September 15, and January 15 of 2027. Miss these, and the IRS charges interest-based penalties on the underpayment.

The simplest way to avoid penalties? The safe harbor rule. Pay at least 100% of last year’s total tax liability, split into four equal payments, and you won’t be penalized even if you owe more when you file. (110% if your AGI was over $150,000.)

Your target is a number you already know.

How to actually pay: IRS Direct Pay is free and instant.

EFTPS works too, but requires advance registration. You can also mail a check with Form 1040-ES, but that’s slower and harder to track.

To make this process painless, start the habit of setting aside 25 to 30% of every payment you receive into a separate savings account earmarked for taxes. Automate the transfer if your bank allows it.

When quarterly deadlines come around, the money is already sitting there.

When Should You Stop DIYing and Hire a Bookkeeper?

It’s time to consider hiring help if bookkeeping takes more than a few hours a month, or if your time is worth more than the cost of outsourcing.

Under $100K in revenue, most freelancers can handle their own books with good software and the weekly routine above. As your business grows, the complexity stacks up. More clients, more transactions, contractor payments, 1099 reporting.

Pay attention to the behavioral signals.

If you’re months behind on reconciliation, if you dread bookkeeping more than your least favorite client project, if you’ve missed deductions or filed late because the books were a mess, those are real signs you’ve outgrown DIY.

And consider the math.

A bookkeeper costs roughly $200 to $400 per month. If your hourly rate is $75 and you’re spending five hours a month on bookkeeping, you’re paying yourself $375 to do work someone else could do for $300. And they’d probably do it better.

The smartest setup for growing freelancers is two professionals: a bookkeeper for ongoing maintenance (categorization, reconciliation, monthly reports) and a CPA for annual tax filing and strategy. Don’t pay CPA rates for bookkeeper work — and make sure your bookkeeper software gives both of you access to the same transactions, documents, and reports.

Start With the Basics and Build From There

Bookkeeping doesn’t need to be the thing you dread. A separate bank account, 30 minutes a week, and a working knowledge of your deductions and quarterly tax obligations covers 90% of it. The other 10% is just consistency.

If you haven’t picked accounting software yet, that’s a good next step.

For everyone else, the better escape from QuickBooks is probably a commercial tool that costs less and does more. Start with our accounting software guide, pick the tool that fits, and get back to the work that actually pays you.

Start simple. Stay consistent. You’ll be fine.

Note: But bookkeeping is only one part of freelance finance. You still need a broader plan for irregular income, cash reserves, insurance, retirement, and the months when client payments arrive later than expected.

Frequently Asked Questions

What is the $400 rule for self-employed people?

If your net earnings from self-employment were $400 or more during the year, the IRS requires you to file a tax return and pay self-employment tax. This tax covers Social Security and Medicare contributions that employers normally withhold from employee paychecks.

What program do most bookkeepers use?

QuickBooks is the most widely used bookkeeping software among professional bookkeepers and accountants. However, many freelancers also use alternatives such as Wave and FreshBooks, especially looking for a simpler or more affordable solution.

What can self-employed people write off?

Self-employed people can deduct many ordinary and necessary business expenses, including home office costs, business mileage, health insurance premiums, retirement contributions, software subscriptions, professional development courses, business insurance, internet expenses, and payment processing fees. The key is keeping accurate records and documentation to support each deduction.

How long should self-employed people keep bookkeeping records?

The IRS generally requires self-employed people to keep tax records for at least three years after filing. However, certain situations can extend that period to six or seven years, so many freelancers simply keep all bookkeeping records for seven years.

When should a freelancer hire a bookkeeper?

Consider hiring a bookkeeper when your bookkeeping regularly falls behind, your business is growing rapidly, or you’re spending several hours each month managing your books. For many freelancers, outsourcing becomes worthwhile once the time spent on bookkeeping costs more than professional help.