The Best Cash Flow Management Tools for Freelancers

You can have your best revenue month ever and still not be able to cover rent.

That’s not a profit problem. It’s a cash flow problem. And most freelancers don’t realize there’s a difference until they’re staring at an empty bank account in a month when they technically “made money.”

Around 82% of business failures cite cash flow as a contributing factor.

For freelancers, the problem is worse than it is for traditional businesses because your income is irregular, your clients pay late, and your tax obligations eat into cash you thought was yours.

The right cash flow management tools — paired with a system that actually works — are what stand between you and that empty-account moment.

Most freelancers only realize how important cash flow management tools are when things start breaking.

This guide covers why freelance cash flow breaks, the system that fixes it, and which cash flow management tools actually help.

Spoiler: the most useful ones aren’t the ones that cost $50 a month.

What’s the Difference Between Cash Flow and Profit?

Profit is revenue minus expenses on paper. Cash flow is actual money moving in and out of your bank account.

You can be profitable and broke at the same time.

Say you finish a $10,000 project in January. Your monthly expenses are $3,500. On paper, you made $6,500 in profit. But the client is on Net 60 payment terms, so you receive $0 in January. Your bank account drops by $3,500 while your P&L says you’re thriving.

This isn’t hypothetical.

According to a Bonsai analysis of over 100,000 freelancer invoices, 29% are paid late. A 2026 report from Jobbers found the average payment timeline across 22,000+ freelancer transactions is 39 days from invoice to funds received.

That’s 39 days where your profit exists on paper but not in your bank.

Your accounting software tracks profit. Cash flow management is about making sure you can actually pay your bills while you wait for that profit to arrive.

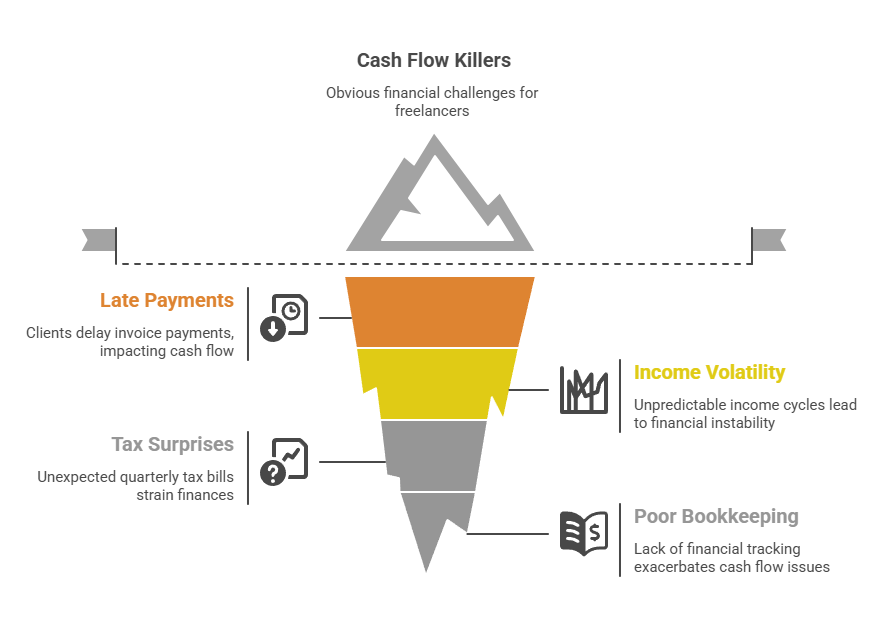

What Are the Three Biggest Cash Flow Killers for Freelancers (and Where Cash Flow Management Tools Help)?

Late-paying clients, feast-or-famine income cycles, and quarterly tax surprises. All three hit harder when you don’t have a system to absorb the impact.

Late payments are the obvious one.

- Freelancers spend an estimated 8–12 hours a month chasing overdue invoices

- Invoices over $20,000 are three times more likely to be paid late than smaller ones

- According to Remote’s Contractor Management Report, 85% of freelancers have experienced late payments at least some of the time

- 40–45% have missed personal bill payments because a client was slow to pay

Then there’s the feast-or-famine cycle.

- One month, you’re turning down work, the next, you’re refreshing your inbox, questioning whether freelancing was a mistake

- 39% of freelancers report struggling to pay bills due to income volatility

- The dangerous part isn’t the famine — it’s that during feast months, most freelancers spend as if the money will keep coming at that rate

Quarterly taxes are the silent killer.

- Self-employment tax is 15.3% of net earnings, on top of income tax

- On $80,000 in net profit, that’s roughly $11,300 in SE tax alone

- If you haven’t been setting money aside all year, the quarterly payment dates hit hard

- New freelancers routinely face a $10,000–$15,000 bill in April with nothing saved to cover it

Good bookkeeping habits make it easier to spot these problems before they become crises. But bookkeeping tracks what happened. Cash flow management is about what’s coming next.

What System Actually Fixes Freelance Cash Flow?

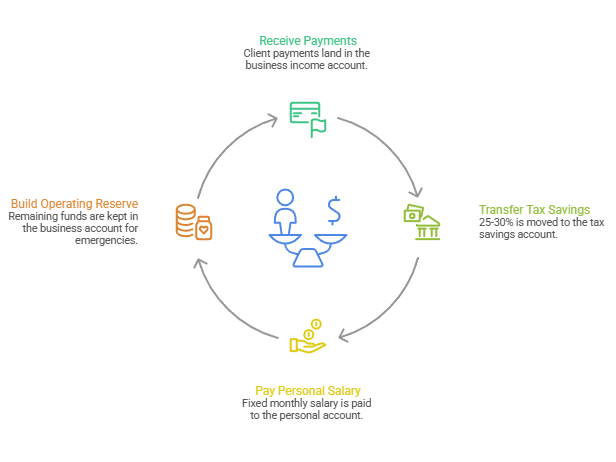

The four-account method: every payment flows into a business income account, then gets split into tax savings, a fixed personal salary, and an emergency reserve. It takes about an hour to set up and removes most of the guesswork.

This is the most recommended system across freelancer communities, financial advisors, and accounting professionals. It works because it forces separation before you can spend.

How the four accounts work

- Business income account — all client payments land here first. This is your intake account, not your spending account.

- Tax savings account — immediately transfer 25 to 30% of every payment. That money doesn’t exist as far as your spending is concerned. It belongs to the IRS.

- Personal salary account — pay yourself a fixed monthly amount. Pick a number based on your second-lowest income month from the past year. Not your average. Not your best month. Your second worst. This doesn’t change month to month regardless of what your business earns.

- Operating reserve — everything that remains stays in the business account. This is what carries you through slow months. Target one month of expenses first, then build to three, then six.

A recent survey found that 39% of small businesses have less than one month of cash reserve. Don’t be in that group.

How to set your salary number

Look at your last 12 months of income, find the second-lowest month, and subtract 30% for taxes. That’s roughly your starting point. Increase it as your reserve grows.

If you’re just starting out and don’t have 12 months of data, use your minimum monthly expenses (rent, utilities, food, insurance, subscriptions) as your baseline and adjust after a few months.

Why this works psychologically

Freelancers with a cash buffer consistently report lower stress and better decision-making, even during slow periods. When you know next month’s salary is already sitting in your account, you stop making fear-based choices about which projects to take.

Cash flow management tools that make it automatic

Relay offers free business banking with up to 20 sub-accounts and automatic percentage-based transfers. Found offers free banking with automatic tax set-asides and “Pockets” for budgeting. Either one handles the splitting for you. Set it up once.

Which Cash Flow Management Tools Are Worth Paying For?

Most freelancers need a good business bank account and their existing accounting software. Dedicated cash flow forecasting tools are worth it only once you’re earning consistently above $75K and juggling multiple clients with staggered payment timelines.

The honest truth from freelancer communities: most people who try dedicated cash flow software end up back in spreadsheets. The system (four accounts, fixed salary, tax set-aside) matters more than the tool. That said, the right cash flow management tools genuinely help at each stage.

| Tool | Price | What It Does | Best For |

| Relay | Free | Banking with sub-accounts and auto-transfers | Every freelancer (the foundation) |

| Found | Free | Banking + automatic tax savings + expense tracking | Tax-anxious freelancers |

| Wave | Free | Accounting with cash flow reports | Budget-conscious freelancers |

| Cushion | ~$8-24/mo | Year-at-a-glance scheduling, feast/famine visibility | Freelancers managing 5+ clients |

| Cash Flow Frog | ~$19-31/mo | 36-month forecasting, what-if scenarios | Growing freelancers ($75K+) |

| QuickBooks Online | $35-99/mo | Cash Flow Planner with projections | Freelancers already on QBO |

| Xero | $20-80/mo | Short-term projections via Analytics | Freelancers already on Xero |

Best foundation for every freelancer: Relay.

Free business banking with up to 20 sub-accounts and percentage-based auto-transfers. This is what makes the four-account system run on autopilot. If you only do one thing from this guide, switch to Relay. Found is the runner-up — pick it if you want automatic tax estimates baked in.

Best for tax-anxious freelancers: Found.

Calculates your estimated quarterly taxes in real time and sets the money aside before you can spend it. If quarterly tax surprises are the thing that keeps you up at night, this is the fix.

Best free cash flow reporting: Wave.

Already free, already does the basics, and the cash flow report is good enough for anyone under $50K in revenue. Pair it with Relay and you’ve spent $0.

For freelancers just testing cash flow management tools without spending money, this is a solid starting point.

Best dedicated forecasting tool for freelancers: Cushion.

The only tool actually built for the freelance feast-or-famine problem. Shows your year at a glance so you can see the December gap coming in October. Worth the $8 to $24/month once you’re juggling five or more clients.

Best for scaling past $100K: Cash Flow Frog.

Proper scenario planning — “what if Client A pays late and Client B doesn’t renew?” — with integrations into QuickBooks, Xero, FreshBooks, and Zoho Books. Don’t bother with this until you actually need it.

Best if you’re already on QuickBooks or Xero: their built-in tools.

QuickBooks Cash Flow Planner and Xero’s Analytics module both do short-term projections that are perfectly fine. Don’t pay for a second tool to do what your accounting software already includes.

Best free option for people who like spreadsheets: Google Sheets.

SCORE offers free 12-month cash flow templates, and a simple monthly spreadsheet takes 30 minutes to maintain. Genuinely good. Not a downgrade.

Run a monthly cash flow check-in regardless of which tool you pick: bank balance plus expected income minus known expenses minus tax reserve equals available cash. That’s your forecast. Write it on a Post-it note if you want.

The system matters more than the software.

Even without advanced cash flow management tools, this habit keeps you in control.

How Do You Stop Chasing Late Payments?

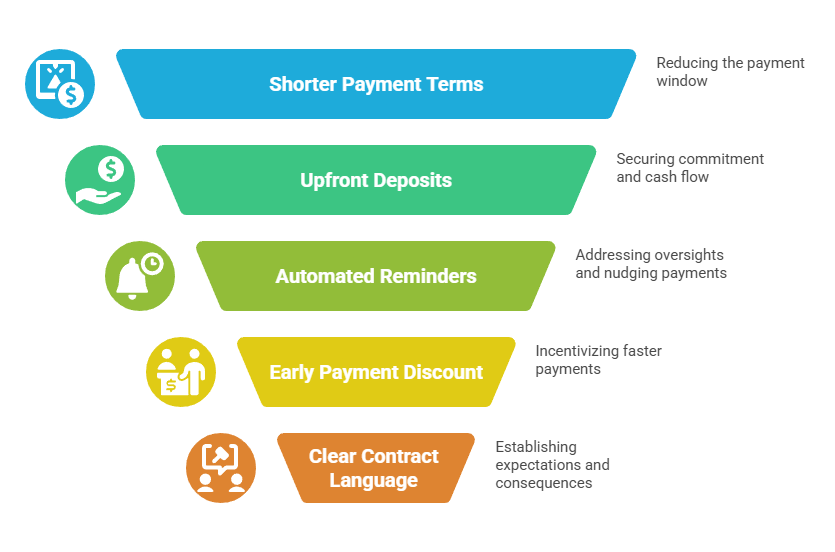

Shorter payment terms, upfront deposits, automated reminders, and clear contract language. Most late payment problems are preventable.

Start with a switch from Net 30 to Net 15.

It sounds aggressive, but most clients won’t push back, and it cuts your average wait time nearly in half. For projects over $2,000, require a 25 to 50% deposit before work starts. This protects your cash flow and filters out clients who were never serious about paying on time.

Turn on automated payment reminders in your invoicing tool. FreshBooks, QuickBooks, and Wave all have this feature. Set reminders for 3 days before the due date, on the due date, and 3 and 7 days after.

Most late payments are oversight, not malice. A polite automated nudge solves the majority of them.

Offer a 2% early payment discount for payment within 10 days. On a $5,000 invoice, that’s $100 off for the client, and you get paid 20+ days faster. The math works in your favor.

And put payment terms in your contract, not just your invoice. Include a late payment fee clause (1.5% per month is standard). You may never enforce it. But having it there sets expectations from the start.

If you’re still figuring out your invoicing process, our guide to invoicing as a freelancer covers the setup in detail.

Get the System Right First

Cash flow management isn’t about finding the perfect app. It’s about building a system that absorbs the unpredictability of freelance income. Separate your accounts, set aside taxes before you see the money, pay yourself a fixed salary, and build a buffer. The cash flow management tools just make the system easier to maintain.

You don’t need to fix everything at once.

The simplest first step?

Open a dedicated tax savings account and start transferring 25% of every payment into it. Today. That single habit prevents the most common freelancer cash flow disaster (the quarterly tax surprise) and gives you a foundation to build on.

From there, pick a salary number, automate the transfers, and stop checking your bank balance every morning. That’s the real goal.

Not a prettier dashboard or a fancier forecast. Just enough structure that money stops being the thing you worry about instead of the work.

Frequently Asked Questions

What’s the difference between cash flow and profit?

Profit is the amount of money left after expenses on paper, while cash flow is the actual movement of money into and out of your bank account. A freelancer can be profitable but still struggle financially if client payments haven’t arrived yet.

What is a cash flow tool?

A cash flow tool helps you track, manage, and forecast the money moving in and out of your business. Depending on the tool, it may help you monitor bank balances, plan for upcoming expenses, set aside taxes, automate transfers, or predict future cash shortages.

What are the best tools for cash flow management?

The best tool depends on your needs. Relay is a strong choice for managing multiple accounts and automating transfers, Found helps freelancers set aside taxes automatically, and Wave offers free cash flow reporting. For more advanced forecasting, tools like Cushion and Cash Flow Frog can help growing freelance businesses.

How much cash reserve should freelancers have?

A good starting goal is one month of business and personal expenses in reserve. As your freelance business becomes more stable, many financial professionals recommend building a buffer of three to six months of expenses.

How to improve cash flow quickly as a freelancer?

The most effective strategies include setting aside taxes automatically, paying yourself a fixed monthly salary, building an emergency reserve, requiring deposits on larger projects, and shortening payment terms to reduce the impact of late-paying clients.